How Your Credit Score Compares with the Average (And How To Improve It)

A credit score is a powerful weapon that can either work for or against you.

The difference of securing a low versus high interest rate on a 30-year mortgage, for example, can affect the whole foundation of one’s financial life. After all, the difference of just 1% on a mortgage of $300,000 is $3,000 in that year. For many people, that might just be their Christmas bonus!

Understanding the different levels of a credit score, and what it takes to improve it, will be a superior tool in your arsenal.

How is a Credit Score Calculated?

A credit score is calculated through the use of a scoring model, of which there are many in use.

This is one reason why credit scores can be a bit confusing; after all, you might have different credit scores depending on where you retrieve your information.

You may have heard of the three credit rating bureaus:

- Experien™

- Equifax®

- Transunion®

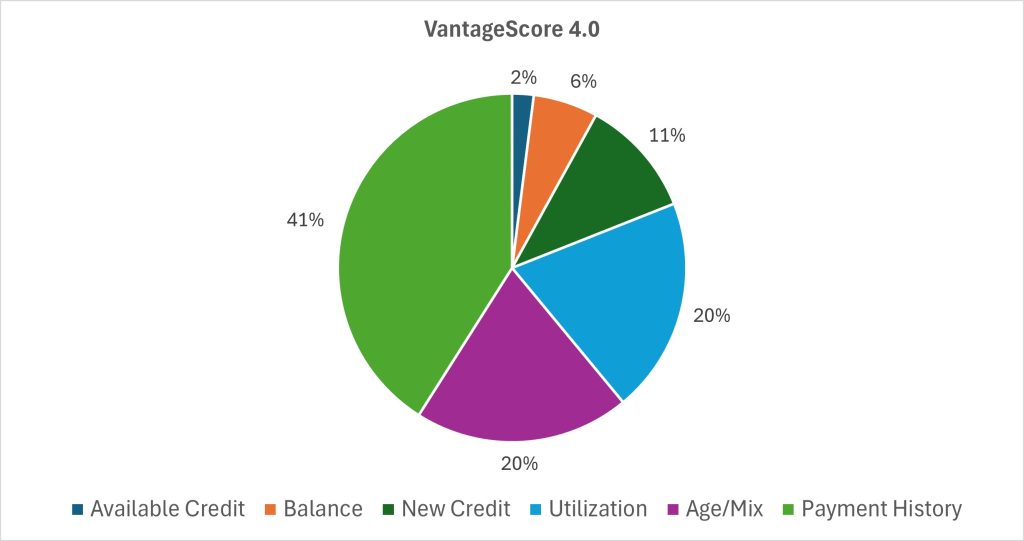

These are the entities which collect and track the data which is subsequently used in a scoring model. Together, they jointly launched a company called VantageScore Solutions, LLC, offering a number of scoring models which includes the latest VantageScore 4.0 (as of 2024).

While the models are flexible depending on each creditor’s history, the VantageScore 4.0 generally weights the data as follows:

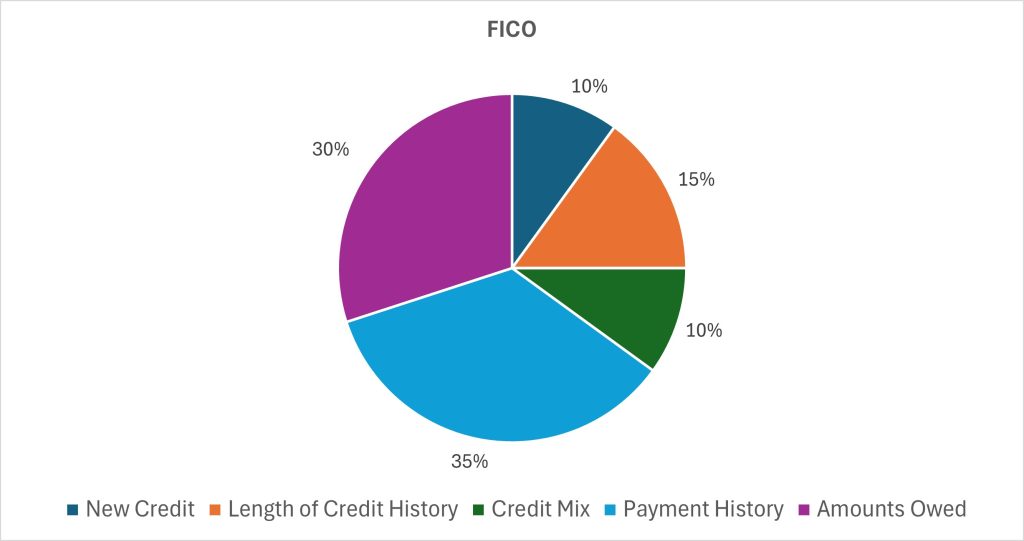

The older and more popular scoring models, however, have been produced by FICO (Fair Isaac Corporation).

The FICO score also uses the input data from the three credit rating bureaus. While it has a variety of scoring models, it generally considers the following data:

The vast majority of lenders prioritize the more traditional FICO score, though they are increasingly referencing the VantageScore as well when making lending decisions.

The 5 Credit Score Levels

The credit score is rated within a range of 300-850, with 850 being the best.

But within this total range, there are five smaller ranges which help lenders categorize borrowers by risk.

Under FICO:

- Exceptional (800-850)

- Very good (740-799)

- Good (670-739)

- Fair (580-669)

- Poor (300-579)

Under VantageScore:

- Excellent (781-850)

- Good (661-780)

- Fair (601-660)

- Poor (500-600)

- Very Poor (300-499)

Because FICO is the more popular rating, let’s use its scoring method to examine what each level means to a lender.

Exceptional (800-850)

This represents those individuals who have a long history of no late payments and low credit card balances. They often have a well-diversified mix of credit, along with low debt as compared with their income.

Very Good (740-799)

Those in this range have a long history of most or all payments being made on time and have low credit card balances relative to the limits.

Very small nuances can make the difference between a very good and an exceptional credit score.

Higher credit utilization (as compared with your limits), applying for new credit, closing old credit cards, and not keeping a diversified mix (credit cards, mortgage, car loans) can keep one in the very good versus exceptional category.

Good (670-739)

The average credit score in the US was 715 in 2023.

The difference between good and very good often comes down to small factors. The main factors might be something like a small number of missed payments in the past or the use of a higher percentage of one’s available credit.

Fair (580-669)

To fall into the fair category, the individual usually has no major delinquencies, but there might be frequent or recent missed payments on record. They might be close to maxing out their credit cards, although utilization over 30% is typically when it starts to work against the score.

Also, if someone has no credit history or a very short one (like students), this can be a big reason for starting out in a lower category.

Poor (300-579)

This one probably needs little explanation.

If someone falls into this category, they probably already understand why.

Maxed out credit cards, delinquent payments, loans being sent to collection agencies, and declaring bankruptcy all can contribute to a poor credit rating. Chapter 13 bankruptcy remains on a credit record for seven years, and Chapter 11 for ten years.

Ways to Improve Your Credit Score

The benefits of a higher credit score include:

- Access to lower interest rates

- Access to more types of loans

- Access to better credit card rewards

- Better insurance rates for car, home and rental

- Better likelihood for being approved as a tenant

- Better financing options (even 0%) for certain expensive purchases

So how do you climb the ladder?

- Perhaps the most obvious is, if you are currently late on a payment, get paid up as soon as possible!

- If you are struggling to make payments, contact the lender and ask what options they have for alternative payment plans.

- Set up all future debt payments, including credit cards, on autopay so that you never miss a payment.

- If you have no credit history, consider starting small with a secured credit card, a student credit card or a credit-builder loan.

- Services such as Experian Boost can report things like utility, phone, rental and insurance payments to the credit bureaus, which can improve your credit score.

- Even if you no longer use a credit card, consider leaving it open unless it has an annual fee. This keeps your debt utilization lower.

- Keep your credit card usage below 30% of its limits.

- Request a credit limit increase from your credit card provider if that will help bring the utilization ratio below 30%.

- Remember that a diversified mix of different types of loans (car, mortgage, credit cards, etc.) show that you can responsibly handle a variety of debts from different lenders.

- Any time you apply for credit, this negatively affects the score temporarily. Don’t apply with multiple lenders without first considering how that could affect your score.

For strategies on how to pay down debt quickly, check out these articles as well:

- Debt Avalanche vs Snowball: 2 Genius Ways to Pay Off Debt Quickly!

- Pay Off Student Loans Quickly With These 8 Strategies

- Is Debt Consolidation a Good Idea?

Conclusion

Remember that when it comes to credit ratings, three things matter with regard to virtually all of these points:

- Recency

- Frequency

- Magnitude

Now that you are aware of the standards, you can map a plan forward.

Debt is a bit like fire: it can be channeled into a useful force or it can burn things to the ground. But if used responsibly, a strong credit score can save a massive amount of money and unnecessary hardship over the years.

And that just leaves more flexibility at your fingertips to build wealth quickly!