Debt Avalanche vs Snowball: 2 Genius Ways to Pay Off Debt Quickly!

Ready to slash multiple debts from your personal balance sheet?

If you have any surplus at the end of a month, let’s investigate the best place to put it. You may have heard of the “debt avalanche” or “debt snowball” strategies. Or you may not have. That’s okay!

These are two very similar strategies that can eliminate debt quickly. Which one you use will depend on which factors are important to you.

Let’s slay some debt dragons!

The Debt Avalanche

The word picture evokes a sense of gathering momentum, growing more powerful as it cascades downhill. That’s exactly what happens with your debt under the avalanche strategy.

This is because the debt avalanche attacks the loans with highest interest first. As each successive debt is paid off, you apply the previous debt’s monthly payments to the debt that’s next in line.

For example, let’s take these three debts and pay them off with the debt avalanche.

Debt A

- Balance: $5,000

- Interest: 7%

- Min Monthly Payment: $100

Debt B

- Balance: $8,000

- Interest: 8%

- Min Monthly Payment: $150

Debt C

- Balance: $12,000

- Interest: 6%

- Min Monthly Payment: $200

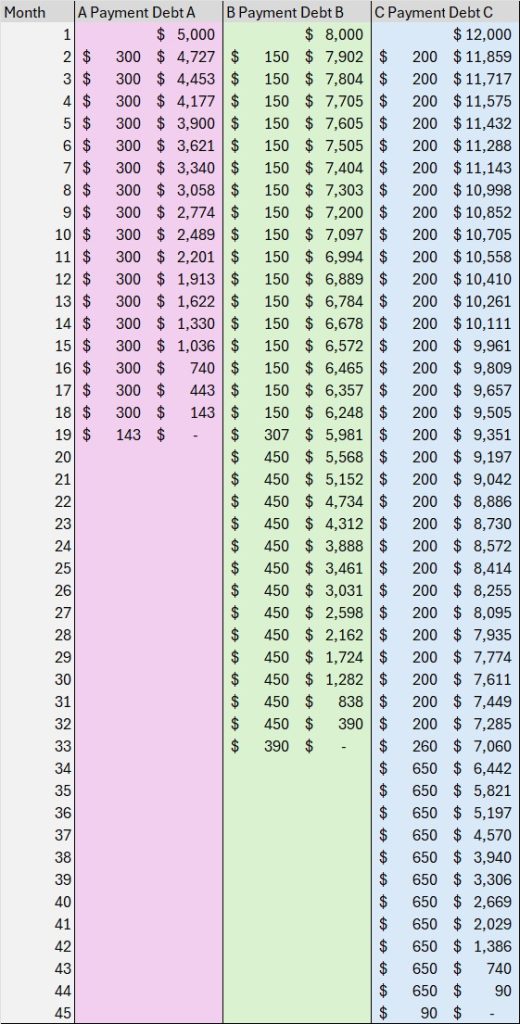

In this case, you would rank them in order from highest interest rate to lowest. That means we would target Debt B first at 8% interest with any excess cash we had at the end of the month. Then we would proceed to pay off Debt A once we eliminated all of Debt B. And lastly, we would apply all of those monthly payments to Debt C.

So let’s say we find $200 at the end of each month which we can apply to this method.

Instead of paying $150 toward Debt B, we would be paying $350 after adding on our extra surplus.

Here’s a visual representation of what this would look like.

In the end, the total cost of principal and interest over this period of 45 months is $27,976.

For comparison, if we had simply made minimum payments on all debts throughout their terms, we would have paid $29,943 over the course of 73 months.

That’s a savings of $1,967, and this strategy has taken the debt off our balance sheet more than two years early!

The Debt Snowball

This picture gives us a sense of consolidation, accumulating a bigger and bigger cash flow quickly.

Whereas the debt avalanche focuses on higher interest first, the debt snowball focuses on smallest debts first.

After all, if we’ve got $200 extra cash flow at the end of the month, why not pay off that $5,000 debt first and free up that cash flow sooner?

In this case, we would pay off Debt A first, followed by Debt B and then Debt C.

Taking an example of what this looks like:

Notice that the difference between the two methods in this case is very insignificant. This still pays off the total debt in 45 months. Total payments combined are $28,041.

That’s only a hair more expensive than the debt avalanche method, a difference of only $65.

With the snowball method, you paid off your first debt in only 19 months instead of 26 as compared with the avalanche method.

And what does it cost you in the end? Only $65 total over 45 months.

Which is Best: Avalanche vs Snowball?

The answer to this question comes down to motivation and capacity.

Ask yourself the following:

- What motivates you more?

- Seeing tangible progress that makes a difference in the here and now? This favors the snowball method.

- Knowing that you are saving as much money on interest as possible? This favors the avalanche method.

- Is cash flow likely to be tighter in the future? This might favor the snowball method in order to free up cash flow sooner in case it is needed.

- How wide is the spread among your interest rates? If it’s 18% on a credit card vs 5% on a car loan, the avalanche method is going to be more significant in the amount it can save you over time.

Conclusion

In summary, remember this simple difference:

The avalanche method will save you money on interest and potentially reduce the time it takes to pay off all loans in totality.

The snowball method will free up cash flow sooner and provide a tangible sense of progress.

Both are excellent ways to tackle debt quickly and save yourself months, or even years, of continuing to pay for yesterday’s purchases.

By applying one of these two simple strategies, just imagine how much faster you can start saving for a liberating tomorrow!