How Much Do I Need to Retire?

“When can I retire?”

It’s a question I’ve heard many times throughout my career. And I imagine it’s a question that everyone asks sooner or later.

After all, according to USAfacts.org, citing the Survey of Consumer Finances, the vast majority of Americans have nowhere near enough in retirement savings to consider early retirement. Most will be depending on Social Security and will probably be waiting until age 67 or 70 to get the most out of it.

Now perhaps you love what you do, and hope to work as long as you can. That’s excellent!

But do you aspire to an earlier retirement, or want to at least have the option to do so? Then let’s take a look at how to plan ahead!

How To Calculate Retirement Needs

Any time we’re trying to plan for the future, we have to make certain assumptions.

The most basic assumptions we have to estimate are:

- Savings rate

- Return on investment

- Social Security / pension payments

- Future expenses

- Future tax rate

- Inflation rate

- Time horizon

Let’s break these down one by one.

Savings Rate

Consider what you are saving toward retirement on an annual basis. Are you contributing to an employer sponsored retirement plan? Don’t forget the company match!

Are you saving additional money into an IRA or other account? Write down the total annual figure.

Also, if you expect your income to increase at least on an inflationary basis, your savings might incrementally increase year-by-year as well. We’ll come back to this thought.

Return on Investment

This is a difficult one to predict over shorter periods (say, 10 years or less). But depending on how one is invested, we can make some broad assumptions, understanding that there is going to be a margin of error.

Let’s use two popular indexes to make an estimate, although this could be different for each person depending on exactly how they have their funds invested.

For the sake of this illustration, let’s use the S&P 500 to represent stock return and NYU’s study of Baa corporate bond returns to represent fixed income.

According to this S&P 500 Return Calculator, the S&P 500 has returned about 10.4% on average, assuming dividends reinvested, from June 1957 to June 2024.

According to New York University’s study on bond returns, the average corporate bond return (rated Baa) has been about 6.8% since 1928. However, I’m going to take the liberty of adjusting this downward, because bond returns can go for very long periods of time with much lower returns if interest rates are low like they were for much of the 2010’s. From the period of 2014-2023, the average return was about 4.7%, so let’s make a compromise and say 5%.

As you can already see, these are very broad assumptions, and the average is not the normal return.

In other words, just because we calculate an average number, the returns are likely to be all over the place on a year-by-year comparison, but likely averaging out to something close to these numbers.

So depending on what asset split you have between equities and bonds, we can make the assumption that average annual returns are likely to be somewhere between 5% and 10% over the years.

Social Security / Pension Payments

Any type of fixed payments that you may be owed should be accounted for. Social Security can be estimated either by going to my Social Security | SSA or using this calculator for a general idea.

Because there has been mention of a potentially reduced Social Security, by a range of 20%-25%, then I prefer to assume that only 80% of the stated estimate will be available. Hopefully this is not the case, but we want to curb our optimism when it comes to government’s ability to responsibly handle finances!

Future Expenses

I often found this was a difficult prediction for my clients to estimate. The best way I have found to calculate this is by considering the following.

If you use a debit or credit card, go through the last 3-6 months of transaction reports. Identify any expenses that are likely to decrease or go away after retirement, and identify any expenses that might actually increase.

For example, mortgages and other debt payments were usually a goal to eliminate before retirement, making a big difference in monthly spending. Also, expenses for kids such as education costs were also usually done by retirement.

But on the other hand, when you no longer have work responsibilities during your day, you will want to fill that time with other things.

And depending on your hobbies, that could cost extra.

For example, are you prone to shop simply to pass the time? Would you go out to eat more often? Do you dream of traveling the world? Are you going to begin some house projects you’ve been putting off? All of these are additional costs that you might not be spending if your days were filled with work responsibilities.

While I don’t have the exact statistics, I felt like it was a coin toss whether my clients would say, “I’m not spending as much as I thought I would,” or “I’m actually spending more now that I’m retired!” This will take some honest introspection to accurately predict.

Future Tax Rate

Tax rates are impossible to predict accurately; we might as well admit that.

Most of the time, we will simply assume that current tax rates continue into the indefinite future, although we know this is not likely to be the case. We simply don’t have enough information to predict what else they would be.

The only time there might be an exception is if we know there is a sunset clause on current tax legislation. For example, we know that the 2017 tax cuts are set to expire in 2025, so we could be more conservative in our estimates by assuming the previously higher tax rates that existed in 2017 will apply in the future.

Inflation rate

Expenses won’t be the same forever. A dollar today won’t buy quite as much as a dollar ten years from now.

The Federal Reserve’s dual mandate is to 1) maintain the inflation rate at an average of 2% per year and 2) maintain maximum employment.

While we don’t know if they can reach this target, we do know what inflation has been historically.

According to the Inflation Calculator, we can learn that over the last 50 years, inflation has averaged about 3.77%. So we know that a target inflation rate of 2% doesn’t necessarily mean we’ll achieve that.

Not knowing the future, we could be ultra conservative and assume that higher rate, or we could make a compromise and assume a middle ground of 3%.

Time Horizon

When we talk about time horizon, we aren’t talking about the time until you need your first withdrawal. That would be considered under liquidity needs.

Instead, time horizon refers to how long any portion of your assets will remain invested. In other words, how long do we need to make your money last?

Assuming your goal is for your retirement assets to last throughout your lifetime, then the time horizon might be equal to life expectancy.

One exception might be in the case of someone who has far more than they will ever be able to spend during their lifetime. Let’s say someone has one or more accounts that they have high confidence will never be touched until their beneficiaries receive the inheritance. In that case, we might stretch the time horizon beyond life expectancy for those particular accounts.

But for the sake of brevity, we’ll stay on track by assuming the time horizon, in many cases, will be approximately life expectancy for anyone using withdrawals to pay for living expenses.

Example of a Retirement Projection

Bringing this all together, let’s look at an example.

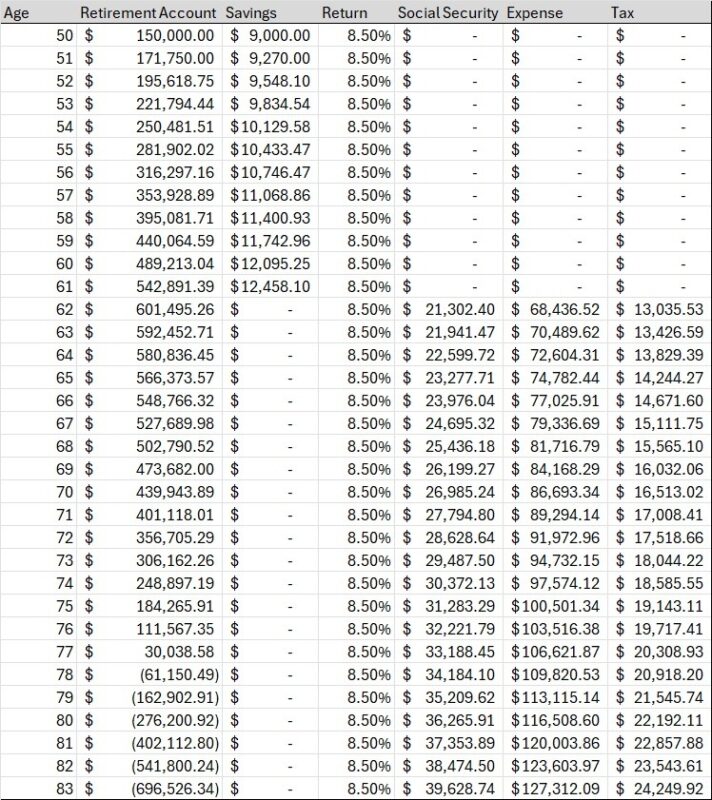

Susan is 50 years old and has $150,000 saved into a 401(k) with her employer. She makes $60,000/year and wishes to know if she can retire at 62.

Here are the assumptions we will make for her:

- Savings rate: $6,000 out-of-pocket, plus a match of $3,000 from her employer

- Return on investment: She is allocated with 70% equities and 30% bonds, so let’s assume (70% equities x 10% avg return) + (30% bonds x 5% avg return) = 8.5% average total return

- Social Security / Pension Payments: $1,775/month

- Future expenses: $48,000/year

- Future tax rate: Assuming 2017 tax rates apply, let’s say we estimate her effective federal tax rate to be 12% and effective state tax rate to be 4%.

- Inflation rate: We’ll pick 3% average inflation to estimate.

- Time horizon: A 50-year-old healthy female has an estimated life expectancy of 82 years.

Plugging this all into an Excel spreadsheet, here we can see that Susan doesn’t quite have enough to confidently make this last until age 82.

Unfortunately, Susan’s retirement assets run out at age 78 and plunge into the negatives. While this is sad to see, it’s also good for us to know so that we can make adjustments now to avoid it.

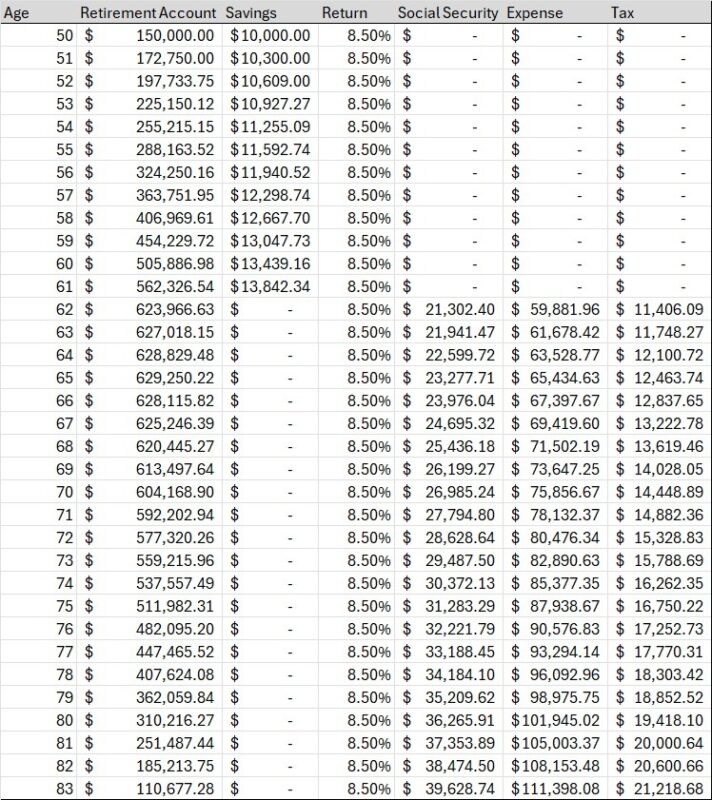

There are a number of assumptions we could adjust, but let’s focus on the one’s we can control.

What if Susan saves $1,000 extra every year up until retirement, and she determines that she could live on a monthly $3,500 instead of $4,000 (assuming today’s dollar values)? Under that scenario, her plan turns out just fine.

The thing about retirement projections is that there are so many assumptions that could work out one way or another.

Social Security could be higher than we’re estimating here.

Susan might get to age 62 and decide she would enjoy continuing to work part-time until 65 or later.

Susan might receive an inheritance.

Susan might get married and share expenses and income with someone else.

Inflation might be below 2%.

Susan might get an unexpected raise or bonus.

Taxes might be lower than we’re estimating.

Return on investment might be higher.

The more assumptions we have, the more uncertain is our final conclusion. So we never want to think of this as a prediction.

Instead, the way to think about this is like a blueprint for how to prudently plan for today. Things will turn out however they turn out, but at least we can do our part today in improving the likelihood of retirement success.

Conclusion

There are a lot of calculations in here, I know.

Don’t let that overwhelm you! This is why there are financial advisors, planners and coaches to help customize this projection on an individual basis.

There are further ways to estimate probability of success, such as Monte Carlo simulations (which we won’t get into here!).

But what I hope you take away from today is that, the earlier you begin your retirement planning, the easier it is to “turn the dials” by making small adjustments here and there, adding up to enormous differences in the future.

My goal with this and future content is to help you achieve your retirement goals, and life goals more broadly, by showing you the tools available and the knowledge of how simple actions can lead to exponentially different futures.

In the end, it’s about giving you the freedom to live life on your terms!