Do Risk-Free Investments Exist?

One of the foundational assessments of financial planning involves the deliberation of the optimal risk level an individual is able and willing to take. The reason for this is that investors can be their own worst enemy when it comes to reacting in moments of stress. The idea of a risk-free investment may sound attractive, but what many fail to realize is that “risk-free” can be a misleading term.

Take, for example, someone who reads about a new conflict breaking out in some region of the world, sees the stock market drop a few percentage points overnight, and immediately decides to go to cash and wait out the volatility until things return to “normal.” While this sounds reasonable on paper, studies show that investors on average give up a massive amount of return over long periods of time because of their tendency to change strategies in this way as a reaction to markets and economies. This, in turn, risks their failure to achieve their long-term goals.

From a long-term investing perspective, if an individual feels the temptation to jump into cash or “safe” investments during volatility, it might be time to reassess what risk is appropriate to take over the longer term. It may also be time to reevaluate the risks involved in the wide variety of investments available.

In the strictest definition of the term, there is no such thing as a risk-free investment. But let’s take a look at the vehicles you can use to get as close as possible.

Cash

What could possibly be safer than cash? While cash is a popular go-to for safety, many people don’t stop to consider the risks involved with cash. Cash loses value over time; the $10,000 you put into cash in year 1 is still $10,000 in year 10, but that same cash value can only purchase a fraction of what it could in year 1 due to compounding inflation. The risk of holding large amounts of cash for too long is that you pay a price for it, even if an invisible one.

That’s not to say that cash doesn’t have its place. While cash loses purchasing power over time, it’s generally a very small erosion over many years before a material difference is noticed (except in rare cases of high inflation). A stock or bond, on the other hand, often has a higher likelihood of losing more in purchasing power over a short- or medium-term period than cash does.

Balancing the odds represents the core of financial decision making. Certainly there will be times when someone beats the odds; one could flip a coin five times and get heads every time. In the same way, someone may even hit a winning streak of beating the odds. But, as with gambling, the odds win out given a large enough sample size.

In other words, cash positions are for short- to medium-term safety. This is usually ideal for situations where you will need to spend the cash within 12 months.

Treasuries

One investment that is often favored for its low-risk nature is a government bond. In the US, this is comprised of:

- Treasury Bills – The shortest maturity period of less than or equal to 1 year.

- Treasury Notes – The medium-term maturity period of 2-10 years.

- Treasury Bonds – The longest maturity of 10-30 years.

Treasuries are backed by the full faith and credit of the US government. For that reason, these securities are often referred to as “risk-free,” since the government has the power to fulfill its obligations either through the Fed’s printing more money or by increasing tax revenue.

While it’s rare to see a government default on its loan, the possibility of course still exists (think Greece in 2015). A government prioritizes debt obligations very highly, and in a tight situation, a government will generally “default” on its payments to government employees or programs before it will default on its loans.

Employees and programs can be made up for in future payments, but once there is a default on a loan payment, the government bonds have suddenly and, almost irreversibly, lost their reputation in the eyes of the world on which their demand depends. That is why, of course, it has happened only very rarely.

Because of the extremely low risk nature of US Treasuries, there is not a great deal of reward in terms of interest. While interest paid can increase, sometimes significantly, this often happens in response to either the presence of, or the future potential of, a higher inflation rate environment. In that way, even if interest rates go relatively high for a time, it’s important to keep in mind the real rate of return.

If a bond is paying 5% interest, but the inflation rate has been 7%, then the purchasing power of the invested cash is still falling behind. On the other hand, if the inflation rate is 2%, then purchasing power is being increased for the present.

Taking this example further, let’s assume interest rates on newly issued bonds are lower than 5%. That means that after maturity of the present bond, the high rate is not able to be maintained without taking on more risk (for example, with “junk” corporate bonds that are more likely to default).

The St Louis Fed tracks the average 10-year inflation-indexed return of Treasuries, which you can view here. As you can see, it’s generally a better real return than cash provides when viewed over several years.

Keep in mind that unless you hold the bond to full maturity, there is the chance that you could lose some money on it if you sell early (if interest rates have risen in the meantime). Interest rates and bond values have an inverse relationship; when one goes up, the other goes down, and vice versa. If you know approximately when you will need access to the cash, you may consider purchasing a Treasury with a maturity date closest to that time.

This is often a good option for cash that will be needed in 1-5 years. Still, there are better potential returns with corporate bonds, but Treasuries are considered “risk-free” as far as governments are able to meet their obligations.

Option Collar

Did you know that you can use options to generate a return with very little, if any, downside?

If options are a foreign concept, feel free to skip this section. This is a more advanced strategy that would not be advisable unless you have a complete understanding of what you’re doing and why. Structuring this incorrectly can be extremely costly.

A collar is a strategy in which the following takes place (in this precise order to avoid as much risk as possible):

- Buy a put option at-the-money on a stock or ETF of your choice.

- Buy the underlying stock or ETF. The quantity should be 100x the number of option contracts you purchased. For example, if you purchased 2 put options, then you would then purchase 200 (2 x 100) shares of the stock or ETF.

- Sell an out-of-the-money call option for approximately the amount to cover the cost of the put option.

Let’s use an example with the following assumptions:

- ETF ticker: ABC

- ETF price: $250

- Put option strike price: $250

- Put option cost: $11.00 (x 100)

- Call option strike price: $260

- Call option proceeds: $11.00 (x 100)

- Both options expire in 9 months from now.

I’ll lay out the way this works.

The first thing to note is that the option strategy in this example has a net zero cost. In real life, there will usually be a very small net cost or net gain at the beginning. The sale of the call option is there to mostly or fully pay for the purchase of the put option.

Because you own the stock, it will either go up or down over these nine months of the strategy, after which you can choose to renew the strategy (purchase and sell more options), sell the ETF, or simply do nothing and assume the risk of owning the ETF.

Because you own a put option at exactly the underlying ETF price (usually you can only get this approximate), then if the ETF has fallen in value by the end of the 9-month period, the option will increase by the amount which the ETF has lost. In this way, the put option acts as insurance against loss.

Remember, owning a put option gives you the option to sell the ETF at the strike price, no matter what the actual price of the ETF does.

If the stock price increases in value, you get the benefit of the upside because you own the stock.

But you only get the benefit of the upside until the price reaches the call option strike price.

Remember, selling a call option obligates you to sell the stock at the strike price. That means if the price goes to $270 by the end of the nine months, the call option (which you will need to buy back or fulfill if you get assigned) will have fallen in value by the amount the stock price has risen above the $260 mark.

What does this do for you? Over nine months, in this example, you have the max potential to earn 4% total return on your investment. That is, $260 / $250 = 1.04.

If the ETF ends exactly where it started, then the only gain or loss to you is the gain or loss it took to sell and buy the options in the first place (very minimal).

If the ETF falls in value, the gain or loss is still equal to the gain or loss that it took to sell and buy the options. That is because you’ve locked in the right to sell your ETF shares at the price for which you bought them.

Is this risk-free? Not completely. There is no guarantee of a gain at the end of the period, depending on what the stock does. There may be a very small loss depending on whether the net trades at the beginning were a gain or a loss to you.

Annuities

There are several annuity products that are issued by insurance companies. A few of the most popular include:

- Fixed annuities – pay a fixed interest rate (tax-deferred) regularly until maturity

- Variable annuities – go up and down with the stock market but are tax-deferred, often allowing for “riders” which can offer various guarantees in the future

- Index-linked annuities – allow for limited potential upside participation in the stock market (tax-deferred) while protecting the downside

While we won’t get into the fine details of each here, the key takeaway is that these often have guarantees from the insurance company that creates these products.

The risk-free nature of these guarantees is only as good as the health of the insurance company. Of course, if the company goes bankrupt, it is possible that they will not be able to fulfill their obligations. While this is extremely unlikely, it does mean that in the strictest definition of “risk-free,” there is still some level of risk, however remote.

One risk of using annuities is the surrender period. Most annuities have a declining “surrender charge” over the years, which means you pay a hefty penalty on the whole value of the account for getting out before those years are up (often ranging between 5-10 years). The risk is that you may need the funds sooner than you thought and end up needing to pay a penalty.

The other risk of using annuities is the opportunity cost of having not invested in something with greater risk but greater potential return. Variable annuities and index-linked annuities often come with high fees for their guarantees; over several years, this can significantly hurt the end value because it lowers the potential compounding rate of return. For example, giving up 2%-3% in fees every year adds up significantly, but that’s the price one pays for guarantees.

The suitability of something like this comes down to the investor’s intentions.

Are they willing to give up a significant opportunity for the benefit of the peace of mind provided by guarantees?

Also, does the annuity provide a valuable sort of middle option between a low-rate Treasury and a volatile stock portfolio?

Depending on goals, time horizon and risk tolerance, annuities may play a specific and useful role in one’s broader plan. If it serves to keep an investor invested, rather than trying to time the market based on speculation, distrust of the financial system, or a combination of fear and greed, then it may be a valuable addition to one’s portfolio.

Certificates of Deposit (CDs)

A Certificate of Deposit (CD) is issued by a bank instead of an insurance company. It is guaranteed by the bank. The Federal Deposit Insurance Corporation (FDIC) also insures up to $250,000 of cash per individual per insured bank, and that includes cash invested in CDs. In other words, anything up to $250,000 is backed ultimately by the government if the bank were to fail.

CDs offer guaranteed interest rates that are generally lower than that of a fixed annuity. They also typically have lower penalties if you have to withdraw the cash before the end of the agreed term.

Interest earned on a CD is taxed in the year it is earned, whereas tax is usually deferred in a fixed annuity to whenever the funds are withdrawn.

The length of the term is often shorter for a CD than that of a fixed annuity. Think of a CD as good for short- to medium-term investing, whereas fixed annuities are better for long-term investments.

Conclusion

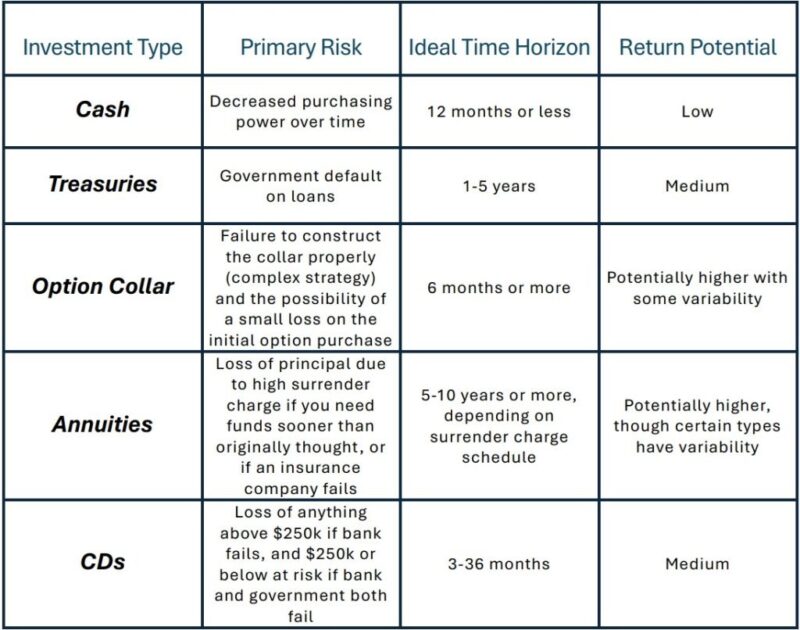

This is not a comprehensive list of assets considered to be low risk, but it offers some of the most popular places that investors tend to go for stability. Here is a useful chart to summarize what we’ve learned.

Of course, everything in a world of limited resources is going to have some measure of risk, no matter how small. If a global Armageddon takes place, then guarantees (not to mention retirement goals) begin to take second place behind the need for shelter, food, clothing and defense. But it’s also important to remember that such disasters are exceedingly unlikely, as well as completely unpredictable in nature, so much so that it hardly can be prepared for with any degree of reasonable action.

That is why, lastly, I will mention one more thing which might be considered low risk.

Living each day to make it count, in a way which leaves nothing to be regretted at the end of one’s life, is a surefire way to know that you are harvesting the reward of life itself without pushing all things too far into the future.

The sacrifice of the present for a better future can be good in small increments. But it’s also important to create a lifestyle around the attainment of the most important goals within a foreseeable timeframe.

Aim to balance the enjoyment of the present with the prudent preparation for the future. In this way, you will reap the rewards of the risks we take every day.

As King Solomon once said, “Hope deferred makes the heart sick, but a desire fulfilled is a tree of life.” Being sure that you can mark specific times in your life when your goals were attained not only builds confidence for the attainment of future and higher goals, but also helps to eliminate the fear of failure. I believe it improves the ability to see and plan more clearly, adding willingness to take on more risk if the capacity and the need is there to take it. It also helps to bring perspective, and to fine-tune future goals to adhere to what you truly desire out of life.

Risk is a fact of life, but knowing how to balance it and rein it in to serve your purposes is the core measure of success in financial planning.